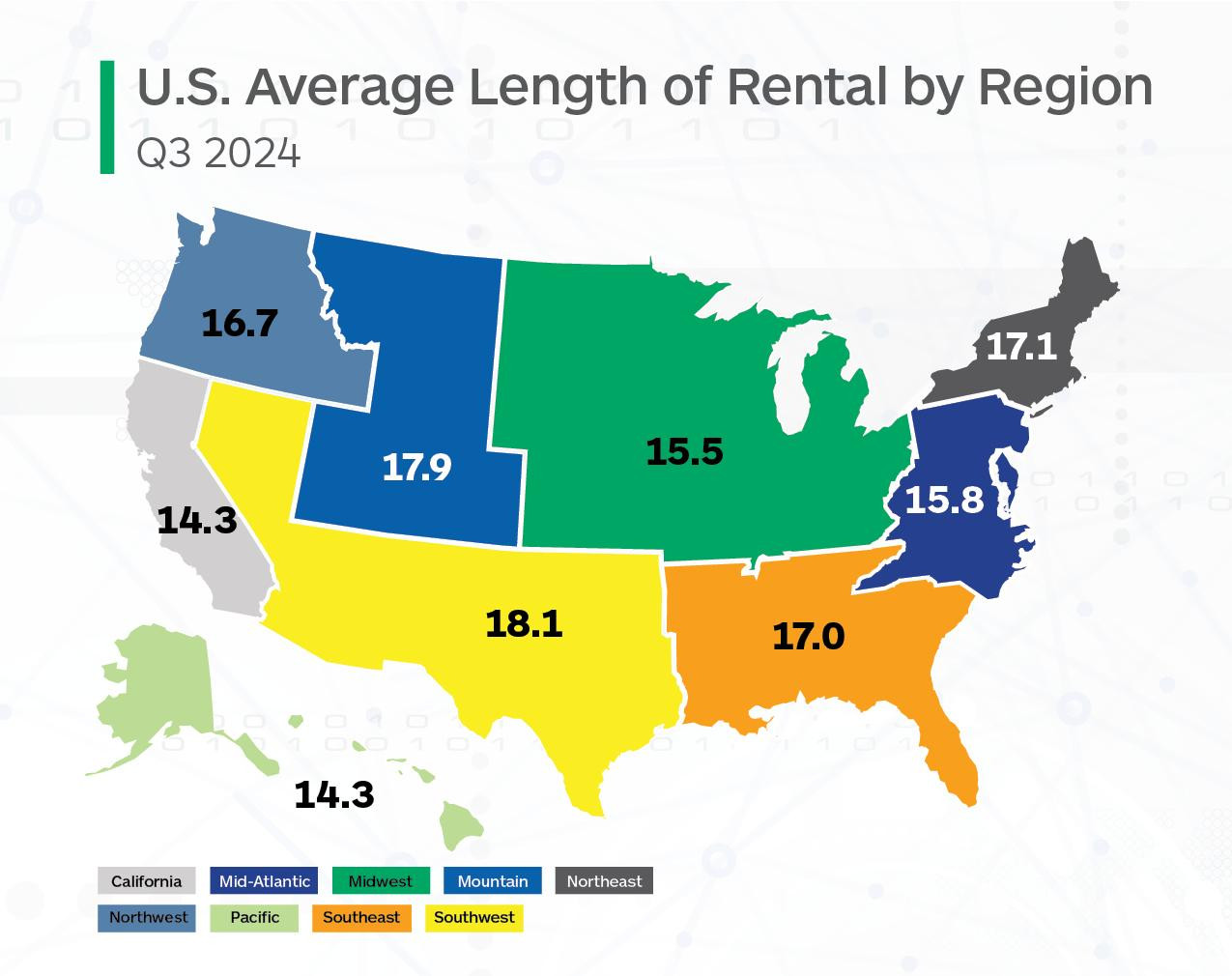

The overall length of rental (LOR) for collision-related rentals continues to decline from 2023’s highs, but remains significantly higher than it was pre-pandemic. According to Enterprise Mobility, which releases quarterly reports, LOR in Q3 2024 was 16.3 days, a 1.2-day decline from Q3 2023.

During 2022 and 2023, many factors affected the collision repair industry, including supply chain issues, parts delays and shifting workforces and driving patterns. However, Enterprise said, it has seen most traditional patterns of LOR return to those last seen in 2021, albeit with overall results higher -- in Q3 2021, LOR was 15.2 days.

As the industry enters the final quarter of 2024, positive signs include lessening backlogs, averted port strikes and lowered supply chain challenges.

While these positives are encouraging, other challenges remain. Significant weather events were prominent in Q3 2024, including hurricanes, flooding, severe weather and hailstorms. Enterprise has also been tracking economic factors impacting customer behavior, such as increased premiums, higher deductibles and claim-filing aversion.

Overall LOR

In Q3 2024, Alaska had the highest LOR at 20.4 days, a 1.5-day drop. New Mexico was second highest at 19.6 days, followed by Colorado (19.5) and Rhode Island (19.5).

North Dakota had the lowest overall LOR at 11.6 days, a 0.7-day decline from Q3 2023. Washington D.C. and Hawaii were joint next-lowest at 12.6 days each, followed by Iowa at 13.3 days.

Oklahoma (17.3 days) recorded the largest drop, down 3.1 days, followed by Washington (-2.6) and Georgia (-2.4). Across 27 states, declines exceeded one full day, compared to the 33 states plus D.C. in Q2 2024. This indicates a slight moderation in the rate of decline. Twenty states plus D.C. saw a decrease of less than one day, compared to 15 states in Q2 2024.

However, Nebraska’s result of 15.5 days represented a 1.3-day increase; several significant weather events in Nebraska during June and July contributed to the increase. Hawaii and Missouri’s results increased minimally by 0.1 day each.

“A continued decline in LOR could be, in part, based on shops’ ability to get repairs started more quickly than they could in 2022 and 2023,” said John Yoswick, editor of the weekly CRASH Network newsletter and an Autobody News writer. “The national average backlog -- how far into the future shops are scheduling new work -- dipped to 2.6 weeks in July 2024, down by less than one day from the second quarter but 1.7 weeks shorter than a year earlier. It was the lowest average backlog of work in any quarter in the past three years.”

Yoswick said in 2019, before the pandemic, typically about 15% of shops reported not having a backlog at all and being able to schedule new jobs immediately.

“The third quarter of 2024 was the first time that specific percentage had rebounded to pre-COVID levels after being less than half that from mid-2021 through the first quarter of this year,” Yoswick said.

However, 18% of the 600-plus shops that reported their backlog in July said they were booked out four weeks or more.

“That’s continued to drop since peaking at 60% in early 2023, but it’s still about twice as many shops as reported that prior to mid-2021,” Yoswick said.

“Several factors are converging to cause a reduction in repairable claims volumes, thus aiding in the ability of shops to efficiently process work in progress,” said Ryan Mandell, director of claims performance for Mitchell International.

“Shops are more likely to better keep up with the flow of work because of some improvements in hiring,” Yoswick said.

Government data shows the industry went on a hiring spree in 2023, and a CRASH Network survey in June indicated stability in employment since then. The total number of full-time workers at 323 shops surveyed was 4,804 people, essentially unchanged from the total number those same shops reported having at the end of 2023.

Almost 2 in 5 shops (38%) said they were fully staffed and not looking to hire -- the highest percentage to say that since the fourth quarter of 2020. Just 24% said that at the end of last year, and only 15% said that in mid-2022.

Greg Horn, PartsTrader’s chief industry relations officer, said the year-over-year median delivery day reduction in Q3 mirrors the LOR reduction.

“Parts are a large influence on repair cycle time and Q3 2023 reflected higher delivery days for OE parts due to the United Autoworker’s strike,” Horn said. “The U.S. collision repair industry and the economy in general were bracing for a potentially damaging Longshoremen’s strike, but the contract was temporarily extended, and the dock workers are back unloading cargo. Now we are focusing on measuring the impact of the hurricanes in the Southeast U.S. in the next quarter.”

Auto insurance premiums continue to increase, with the Bureau of Labor Statistics reporting a 16.5% increase in August compared to the same month last year, and 0.4% over July. Consequently, average first-party deductibles continued to rise in Q3, with the U.S. reaching an average of $834 -- up 20.7% compared to Q3 2023 and 1.1% compared to Q2 2024.

Drivable

In Q3 2024, drivable LOR was 15.1 days, down 0.6 days from Q3 2023. Compared to Q3 2021, LOR is flat, as the result then for drivable LOR was 15.2 days.

Alaska had the highest drivable LOR in Q3 2024 at 18.9 days, a minor 0.3-day drop from Q3 2023. Colorado was next highest at 18.6 days, followed by Rhode Island (18.2) and New Mexico (18.1).

As with the overall results, North Dakota had the lowest drivable LOR at 10.2 days, a 0.1-day decline. Hawaii (11.1) and D.C. (11.5) were the two next-lowest results.

As seen in the overall numbers, Oklahoma had the largest decline, dropping 2.2 days from 18.6 to 16.4. Mississippi had the second-largest drop, down 2.1 days from Q3 2023. An additional six states had a decline greater than a full day.

At the opposite end, Nebraska’s results increased by two full days in Q3 2024. Missouri (15.8) saw an increase of 1.3 days, while West Virginia’s (16.4) results were up 0.9 days. Eight additional states saw an increase, while five other states had flat results.

Non-Drivable

Non-drivable LOR was 22.3 days in Q3 2024, a 2.7- day decline from Q3 2023. For comparison, non-drivable LOR was 21.9 days in Q3 2021.

As with overall and drivable results, Alaska had the highest LOR at 30.4 days, which was still a 2.1-day decrease from Q3 2023. West Virginia was next highest at 28.8 days, followed by New Mexico and Vermont, each at 27.1 days.

D.C. had the lowest LOR at 18.1 days, representing a 3.0-day decrease. North Dakota was next lowest at 19.1 days, followed by California at 19.9 days.

South Dakota had the highest decrease with results of 21.1 days representing a sizable 7.9-day decline. Washington (23.3) had results lower by 6.7 days, while Oklahoma (23.4) was lower by 6.2 days. Thirty-six states, plus D.C., all had decreases greater than two days.

Only one state, Vermont (27.1), saw a non-drivable increase, up 0.3 days.

Yoswick said the average time shops have had to wait for an insurer to review a supplement has declined over the past year.

“While the improvement amounts to less than half a day, it marks the first year since 2019 that average wait times have declined at all,” he said.

“Across all 12 insurance carriers asked about in CRASH Network’s survey in June, shops say they are waiting 4.9 days on average for an insurer to complete an in-shop inspection to approve supplements,” Yoswick added. “That is down from the 5.4-day average reported in 2023, but still well above the 2.9-day average wait time reported in 2018. Wait times for a remote or ‘virtual’ review are averaging 4.3 days among those same insurers, only slightly shorter than the 4.6 days reported a year ago.”

Total Loss

LOR for rentals associated with a total loss claim was 14.9 days, a 1.7-day decrease. Compared to Q3 2021, LOR was 16.2 days -- making Q3 2024 total loss LOR the only result to see a decrease compared to Q3 2021, with 2024’s results lower by 1.3 days.

West Virginia had the highest total loss LOR at 19.0 days, a 0.9-day increase from Q3 2023. New Mexico was next-highest 18.7 days, followed by Wyoming at 18.3 days.

North Dakota had the lowest total loss LOR with 11.6 days, with D.C. (12.6) and Iowa (12.9) next-lowest.

Alaska (15.9) had the highest decrease at 7.5 days, with D.C.’s results of 12.6 days representing a 5.1-day decline. Sixteen additional states had declines greater than two full days.

Wyoming’s LOR of 18.3 days was up 1.1 days, with West Virginia (19.0) up 0.9 days and Kansas (15.2) up 0.3 days; these states were the only increases.

New Mexico’s (18.7) results were unchanged from Q3 2023.

“Total loss frequency is also increasing as vehicle values continue to gradually cool, with the U.S. reaching 20.6% in Q3 2024, compared to 18.4% in Q3 2023,” Mandell said.